- There are many ways to finance healthcare, including insurance, savings accounts, BNPL, provider plans, loans, government programs, and negotiation strategies.

- Choosing the right medical financing option depends on the patient’s credit profile, urgency of care, and long-term financial goals. Comparing terms, interest structures, and repayment timelines is key.

Medical costs have been rising steadily, and insurance coverage doesn’t always go far enough. According to one survey, 79 million Americans struggle to pay medical bills or deal with healthcare-related debt. Even with insurance, patients are often left covering high deductibles, elective procedures, and treatment from out-of-network providers.

Whether you’re a patient facing an unexpected medical emergency, or a provider trying to make it easier for your patients to cover elective procedures like LASIK or dental implants — there are many ways to finance medical care without sacrificing financial stability. This guide walks you through the most common — and creative — financing options available today.

What Is Medical Financing?

Medical financing refers to the process of allowing patients to spread the cost of healthcare services over time through structured installment plans, loans, or lines of credit. It’s commonly used for elective or out-of-pocket procedures not covered by insurance — like cosmetic surgery, dental work, and med spa services. By partnering with third-party financing providers, healthcare practices can offer their patients greater financial flexibility, improve access to care, and increase treatment acceptance rates.

Health Savings Accounts (HSAs)

HSAs are tax-advantaged savings tools available to people with a qualifying high-deductible health plan (HDHP). They allow consumers to set aside pre-tax money to pay for qualified medical expenses — from copays and prescriptions to dental, vision, and even certain mental health services.

The money rolls over year to year and can be invested, growing tax-free. HSA funds can be used at any time for qualified expenses, even if the account holder changes jobs or health plans.

Pros:

- Tax-free contributions, growth, and withdrawals

- Funds roll over and grow over time

- Can be used for a wide range of qualified expenses

Cons:

- Only available with high-deductible health plans (HDHPs)

- Contributions are capped annually

- Not helpful for patients who need immediate large sums

Tip: Many people don’t realize that, because of the expansion of the CARES Act, HSA funds can be used for over-the-counter items, alternative treatments like acupuncture, and long-term care insurance. They're also a great backup retirement tool: after age 65, withdrawals can be used for non-medical purposes without penalty (though income taxes apply).

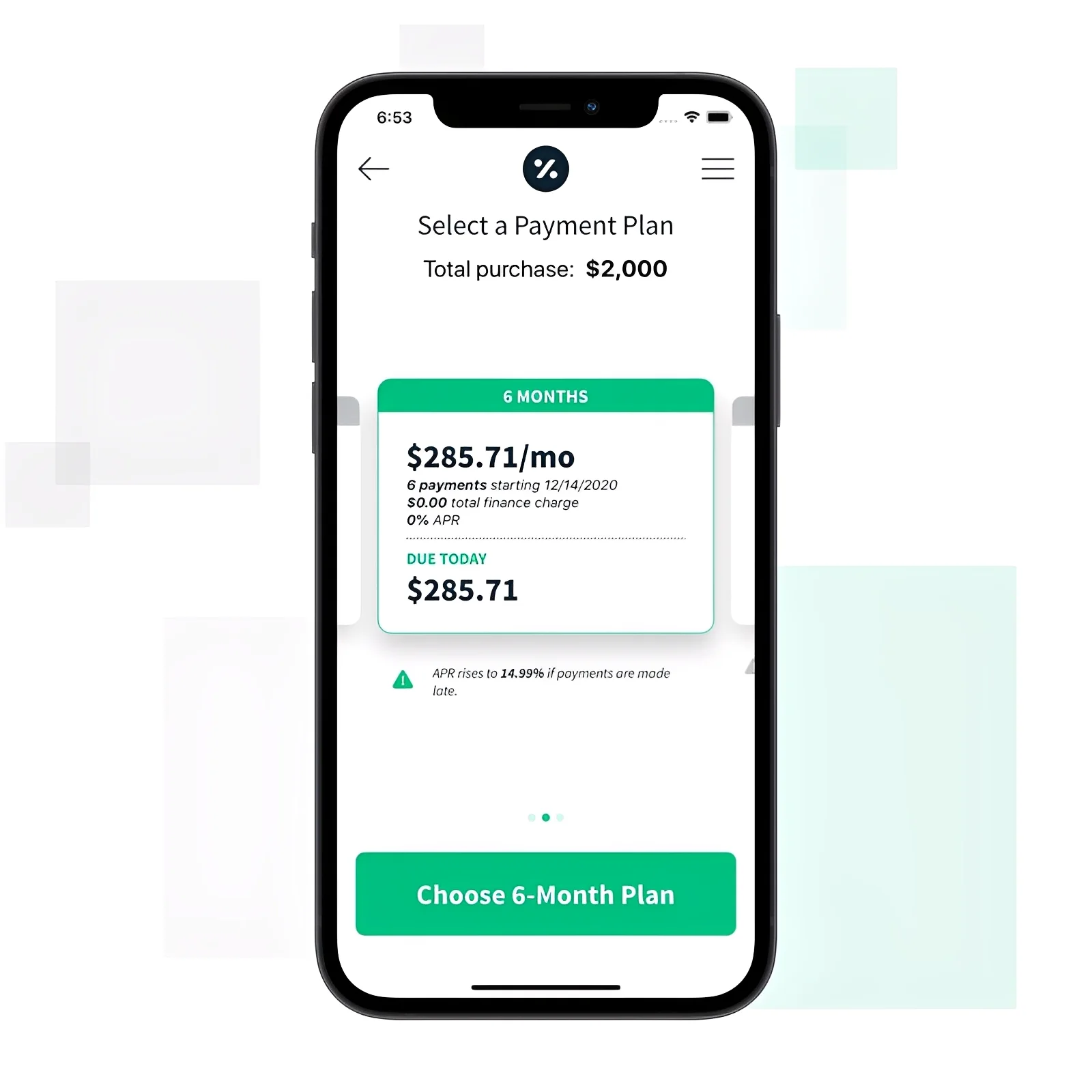

Buy Now, Pay Later (BNPL) for Healthcare

BNPL services made popular by companies like Klarna and Afterpay are being increasingly used in the healthcare space. They allow patients to pay over time by splitting the total cost of a procedure into smaller, manageable installments.

With Cherry Payment Plans, for example, bills can be split into monthly or weekly installments with interest-free payments for short-term plans, and qualifying 0% APR for longer-term monthly plans. Unlike other leading providers, Cherry approves borrowers from a wide variety of backgrounds with both good and bad credit, and never conducts a hard credit check or charges deferred interest.

Pros:

- Easy and fast approval process (Cherry offers a 35-second application and borrowers will see loan offers upon approval)

- Instant approval decisions at the point of care

- Often no hard credit check during the application process (no harm to credit score)

- Instant funding upon approval, making immediate checkout possible

- Ideal for elective procedures not covered by healthcare

- Upfront payment to practices

- Good alternative to high-interest options that can lead to medical or credit card debt

- Flexible loan options (Cherry offers up to $50,000 in funding and terms from 1-60 months)

Cons:

- May charge late fees or simple interest if payments are missed

- Limited to participating providers or platforms

Tip: Approval is often fast, sometimes same-day, and some platforms, like Cherry, don’t require a hard credit pull (allowing patients to search for the lowest rate without hurting their credit report). Missed payments may incur fees and could hurt patients’ credit score if reported to credit bureaus. On the other hand, on-time loan repayment can help borrowers improve their credit profile — which is not always possible with other financing options.

Medical Loans

Medical loans are loans specifically used for healthcare expenses. While they function similarly to traditional personal loans, they’re often offered by companies that specialize in healthcare financing and may offer tailored features — like working directly with healthcare providers or offering fast-track funding for urgent care. Medical loans can be used for a wide range of procedures, including elective surgeries, dental work, fertility treatments, or even consolidating multiple medical bills into one monthly payment.

Pros:

- Specifically designed for healthcare-related expenses

- Can cover elective procedures not typically covered by an insurance company

- May help consolidate multiple medical bills into one loan

Cons:

- Interest rates may be higher for borrowers with poor credit

- Some loans include origination fees and prepayment penalties

- Requires a credit check, which can affect the patient’s credit score if it’s not a soft pull

Tip: Before taking out a medical loan, patients should ask their provider if they partner with any specific lenders — this can streamline the application process and sometimes unlock better terms.

Medical Credit Cards

Medical credit cards like CareCredit or Alphaeon Credit are designed specifically for healthcare expenses. These cards often feature interest-free promotional periods — such as 6, 12, or 24 months — if the balance is paid in full by the end of the term.

However, if a payment is missed or if even $1 remains unpaid on the balance at the end of the promotional period, interest may be charged on the entire purchase amount from the beginning (this is called deferred interest).

Medical credit cards are widely accepted at medical, dental, veterinary, and cosmetic clinics, and approval decisions can be made within minutes.

Pros:

- Often offer 0% interest for a promotional period

- Easy to apply and use for healthcare-specific expenses

- Accepted at many providers

Cons:

- High deferred interest if not paid on time

- Will affect credit score with a hard credit check

- Not suitable for large balances if they can’t be paid off quickly

Tip: Deferred interest may apply retroactively, sometimes at rates over 25%. The Consumer Financial Protection Bureau considers deferred interest to be a significant risk to consumers. Make sure to budget carefully or explore fixed-rate installment plans as an alternative.

Personal Loans

Personal loans are a versatile way to finance medical treatment. Patients receive a lump sum upfront, repayable in fixed monthly payments over a set term — usually between 12 and 84 months. Personal loans are unsecured loans, meaning the patient doesn’t need to offer collateral.

Personal loans can be applied for through a bank, credit union, or online lender. If the borrower has good credit, they may qualify for competitive rates, high loan amounts, and flexible loan terms. Lenders may also offer fast approval with direct deposit of loan funds, sometimes the same business day.

Pros:

- Fixed interest rates and repayment terms

- Can be used for almost any medical expense, including a refinance or debt consolidation

- Higher borrowing limits than credit cards

Cons:

- May require good credit for low rates

- Origination fees and prepayment penalties may apply

- Adds to long-term debt burden

Tip: Compare APR (annual percentage rate), not just interest rate, to see the true cost of borrowing. Also review for hidden fees, including origination fees, late payment fees, or prepayment penalties.

Provider Financing Plans

Some healthcare providers offer their own in-house financing or partner with third-party financing services to offer monthly payment options. These are common in dentistry, dermatology, plastic surgery, fertility clinics, and med spas. These plans may offer no-interest periods or extended terms, and some even allow patients to pre-qualify with a soft credit check.

Pros:

- Often interest-free or low-interest

- May not require strong credit

- Streamlined through the provider’s office

Cons:

- Limited to participating providers

- May still require a down payment

- Approval and terms vary by provider

Tip: Ask about the terms before treatment begins — including interest rates, late fees, and the impact of missed payments. These plans are often more flexible and accessible than traditional loans, particularly for people with fair or limited credit history.

Home Equity or Credit Lines

If the patient owns a home, a home equity loan or home equity line of credit (HELOC) allows them to borrow against their equity at relatively low interest rates. These loans offer larger borrowing limits, longer repayment terms, and are ideal for expensive treatments or long-term care.

Pros:

- Low interest rates due to secured nature

- Can borrow large amounts for major procedures

- Long repayment terms available

Cons:

- Requires home ownership and equity

- Risk of foreclosure if the patient defaults

- Application process can be lengthy

Tip: Because these are secured loans, the patient’s home is used as collateral. Failure to repay could result in foreclosure, so they should only choose this option if they’re financially stable and confident in their repayment plan.

Government Assistance Programs

Programs like Medicaid, Medicare, the Children’s Health Insurance Program (CHIP), and state-specific offerings provide low- or no-cost care for eligible populations. They cover essential services including doctor visits, hospitalizations, lab tests, and prescription drugs.

Pros:

- Free or low-cost coverage for those who qualify

- Covers a wide range of essential services

- No repayment or interest

Cons:

- Strict eligibility criteria

- Long application process

- May not cover all providers or procedures

Tip: Each program has specific eligibility criteria based on income, age, or disability status. The application process can be lengthy and may require documents like tax returns, pay stubs, and a credit history check (for income verification purposes). But if the patient qualifies, the savings can be substantial.

Medical Expense Reimbursement Plans (MERPs)

MERPs are employer-sponsored programs that reimburse employees for eligible medical procedures not covered by traditional insurance — such as deductibles, co-pays, or even premiums. Unlike HSAs, MERPs are funded and managed by the employer.

Pros:

- Employer-funded and tax-advantaged

- Customizable to employee needs

- Helps bridge gaps in standard insurance

Cons:

- Only available if offered by the patient’s employer

- Reimbursement process may be slow

- May not cover all types of expenses

Tip: MERPs are fully customizable — some may only reimburse a few types of expenses, while others cover a broader range. The patient should ask their HR rep for the plan’s disclosures and requirements for submitting receipts or documentation.

Negotiating Medical Bills

Many people don’t realize they can negotiate healthcare costs — often with surprising results. They should start by requesting an itemized bill and reviewing it for errors. They can ask for a cash discount, request a payment plan, or explore financial assistance options through the provider.

Pros:

- Can significantly reduce costs

- Often results in better payment terms

- No interest or credit required

Cons:

- Time-consuming and requires persistence

- Not always successful

- A portion may need to be paid upfront

Tip: Hiring a medical billing advocate may be worth the investment for complex bills. They understand healthcare pricing, billing codes, and how to challenge inflated or erroneous charges effectively.

Nonprofits and Crowdfunding

Nonprofits and online platforms can help those who struggle to qualify for traditional loans or are overwhelmed by medical debt. Organizations like HealthWell Foundation, Blood Cancer United, or CancerCare provide grants or direct payment to providers. Platforms like GoFundMe allow patients to raise money from friends, family, and their community.

Pros:

- May provide financial aid with no repayment

- Community support can offset large expenses

- Ideal in times of crisis or unexpected needs

Cons:

- Not guaranteed or predictable

- Public sharing of personal health info may be required

- May not cover full costs

Tip: The campaigns that have the most success are honest and personal. Photos, detailed descriptions, and regular updates help to improve visibility. Some platforms offer fundraising FAQs and marketing tools to help improve campaign success rate.

Health Insurance Coverage

Health insurance is the foundational tool for covering medical costs. Offered through employers, government programs like Medicare or Medicaid, or the ACA marketplace, it typically pays for doctor visits, emergency care, prescriptions, and hospital stays. Most policies also include preventive care at no cost to the patient.

Policies vary widely though. Some require patients to meet a high deductible before coverage kicks in, and others may not cover procedures from out-of-network providers or elective treatments like cosmetic surgery, medical aesthetics, or fertility treatments (e.g., IVF). Understanding eligibility, plan benefits, and exclusions is crucial.

Pros:

- Covers a wide range of medical services

- Can significantly reduce out-of-pocket expenses

- Often includes preventive care and prescription benefits

Cons:

- May not cover elective or cosmetic procedures

- High deductibles and copays can still be costly

- Limited provider networks can restrict access to care

Tip: Look into supplementary insurance policies, such as critical illness insurance, dental or vision plans, to expand coverage.

Personal Savings

Using personal savings is the most straightforward way to pay for care. There's no credit check, loan application, or interest to worry about. If the patient has planned ahead, they can tap into their personal funds or designated healthcare savings account for predictable costs like LASIK, dental implants, or an expected surgery.

However, for large or sudden expenses, dipping into savings can drain not just their emergency fund, but money earmarked for other goals like housing or retirement.

Pros:

- No interest or debt accumulation

- Immediate access to funds

- No application or approval required

Cons:

- May deplete savings or checking account

- Not feasible for major or ongoing treatments

- Opportunity cost if funds could be invested elsewhere

Tip: Try setting up an automatic transfer to a separate medical savings fund. Even small amounts saved monthly can make a big difference when unexpected costs arise.

Medical Financing FAQs

1. How should patients evaluate different patient financing options?

When comparing patient financing options, patients often look beyond the monthly payment and interest rate. It helps to consider how long payments will last, whether the approved amount fully covers the cost of care, and how payments fit into day-to-day cash flow. Many online lenders offer a loan calculator to help patients compare loan rates and understand the total cost before committing.

2. Can patients with insurance still use patient financing?

Yes. Patient financing is commonly used alongside all types of healthcare plans, including employer-sponsored insurance, Medicare, Medicaid, and Affordable Care Act plans. Even with coverage, patients may still be responsible for deductibles, copays, coinsurance, or services that aren’t fully covered. Financing helps manage those remaining costs, especially as health insurance premiums and out-of-pocket costs continue to rise.

3. What are the main types of patient financing solutions, and how do they differ?

Patient financing includes several common ways patients pay over time, and the right fit usually depends on the size of the expense and how quickly the patient wants to repay it.

- Buy Now Pay Later options: Let patients split healthcare payments into equal, predictable installment payments. Many BNPL options offer short-term interest-free plans and more flexible approval criteria. Healthcare-specific BNPL providers, like Cherry, support higher loan amounts and longer terms.

- Healthcare credit cards or credit lines: Provide revolving credit that can be reused for future care. These products are ideal for ongoing treatment, but often come with lower funding limits and deferred interest traps.

- Installment loans: A fixed loan amount repaid over a set schedule with predictable payments. Patients can access these through a bank, credit union, or an online lender like SoFi. Some lenders offer personal loans designed specifically for healthcare purchases.

4. Can caregivers help manage medical financing for a loved one?

Yes. Caregivers often help a loved one review financing options, understand eligibility requirements, and manage patient payment schedules — especially during recovery or ongoing treatment. This support can ease financial stress and reduce confusion around healthcare payments.

5. Can patients combine financing with patient assistance programs from nonprofit organizations?

Yes. Some patients are eligible to reduce what they owe through outside financial assistance programs, such as charity care offered by nonprofit hospitals. After that support is applied, financing can be used to cover any remaining balance. This approach can be especially helpful for low-income patients facing a larger financial burden.

6. How should medical providers decide which financing options to offer?

Patient experience is often a key factor when medical providers evaluate financing options. Practices typically consider how easy an option is for patients to understand, how approvals work, and whether the solution fits smoothly into existing billing department workflows. Providers also look at costs to the practice, including merchant fees and whether payment is received upfront, as well as how financing affects patient satisfaction over time. Generally, the financing option the practice chooses should both help the practice grow while offering patients affordability and peace of mind.

7. Do you need a good credit score to qualify for patient financing?

Not always. While traditional financial services companies use narrow eligibility criteria, modern patient financing programs approve applicants across a wide range of credit profiles. While stronger credit may qualify someone for lower interest rates or longer repayment terms, others may still be approved for manageable payment plans. Comparing options ahead of time can help patients choose a payment method that fits their budget.

8. Why should healthcare practices offer flexible payment options?

Offering financing helps healthcare practices improve treatment affordability and access to care. When patients have flexible payment plans available, they’re more likely to move forward with recommended treatment. Payment flexibility supports more predictable collections and smoother operations for the practice, and can also make conversations about cost easier for staff.

Offer Flexible Medical Financing With Cherry

From standard insurance to credit cards, loans, BNPL, and financial assistance, there is no one-size-fits-all solution to paying for healthcare. The best choice depends on the patient’s creditworthiness, income, medical needs, and how quickly you need the funds.

At Cherry, we can help you offer flexible financing to patients of all backgrounds — even those who may not meet traditional credit approval standards. We approve up to 90% patients for financing — 78% more than the industry average.

No matter what medical procedure they need financed — from dental care to veterinary — our wide range of terms (1-60 months), flexible loan amounts (up to $50k), and true qualifying 0% APR for monthly plans allow more patients to say “yes” to the treatment they need. Applying and getting an approval decision takes less than 35 seconds and doesn’t hurt credit score, and providers can generally integrate our system the same day.

Get paid for treatment upfront, pay the lowest merchant fees in the industry, and let us handle the rest. Find out why over 50,000 medical practices choose Cherry as their preferred financing partner over 80% of the time. Book your free demo today.